Yen Collapse: How the Japanese Central Bank Continues to Commit Treason

Why the yen will remain weak despite massive intervention, and what is behind the BoJ’s weak yen policy

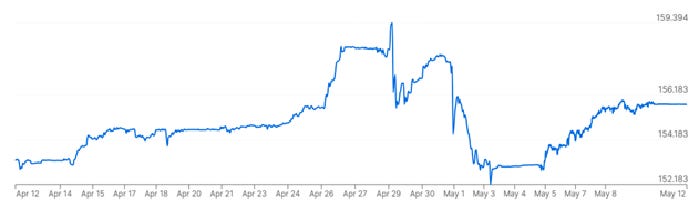

20 May 2024. Tokyo. Once again, events surrounding Japanese monetary policy are a key focus of world financial markets. The Japanese yen, having recorded several 34-year lows against the US dollar this year already, dropped sharply again in late April. Then, on 29 April 2024 the fall turned into a collapse, within a few hours marking down the Japanese currency by several yen, to a low of Y160.04/$. This was not far from the prior weakest point more than 37 years ago in April 1990 (at Y160.33/$). If the yen had breached this point, the currency collapse could further accelerated, as market traders would be betting on a move to the next pivotal levels of Y174/$ or even Y239/$. However, the yen sharply reversed at this crucial point – likely triggered by foreign currency intervention ordered by the Japanese Ministry of Finance.

So after it had dropped below the $160/$ line, the yen reversed sharply and appreciated, moving almost as high as Y152/$ within a few hours.

However, within two days the yen had fallen back again and headed to as low as Y158/$. The game was replayed on 1 May, when the yen dropped dramatically again, only to take another U-turn and recover abruptly. As before, the reversal was likely triggered by a second bout of official FX intervention, which would be more effective on a day that is a holiday in many countries, as 1 May is, and hence transaction volumes are lower than on ordinary days. This boosted the yen back to a temporary peak of Y151.87 on 3 May.

After such dramatic moves and reversals, the yen has since gradually drifted lower once again, settling in the Y155/$-157/$ range, but leaving many to wonder whether it will soon once again challenge the Y160/$ threshold.

Official Intervention

When the yen weakened to beyond Y160/$, this is likely the moment when Masato Kanda, my fellow student of the Oxford MPhil economics, year of matriculation 1989, gave the formal instruction to the Bank of Japan to implement official currency intervention for the first time since 2022. In that year the yen first plunged beyond Y134/$ in June 2022, and then to lows near Y152 per dollar in October 2022. At that time the Ministry of Finance was estimated to have spent ca. Y9.2 trillion (ca. $61 billion) defending the currency – to little avail. This did not stop many currency forecasters from predicting a stronger yen, since, no doubt, it became unusually cheap.

In 2022 as well as this year, Masato-kun likely gave the instructions to the Bank of Japan to sell official US dollar holdings and purchase Japanese yen on the government’s account. When it comes to the official foreign exchange reserves, the central bank merely acts as the agency broker for the government. Masato Kanda is the present vice minister for international finance at the Ministry of Finance (also often translated more formally as “vice minister of finance for international affairs”), the position that often causes the incumbent to be called “Mr Yen” (as in the case of the vocal Eisuke Sakakibara, who was in this job in the tumultuous late 1990s). The Ministry of Finance is, by law, the institution in Japan that exercises the government’s prerogative to manage the country’s foreign exchange reserves and the holder of this job is the most senior official in charge of this task, including the decision of when and how to deploy the reserves to intervene in the FX markets. He is technically subject to instruction by the Minister of Finance, but that rarely happens.

Keep reading with a 7-day free trial

Subscribe to Richard Werner’s Substack to keep reading this post and get 7 days of free access to the full post archives.